Having a moderate income does not mean that you have to live like a pauper.? If you want to live well, then the key is living within your means.? That means not stretching the family budget to upgrade to a larger home that you can barely afford, or trading up for a new car every few years.? A few small sacrifices here and there on your more big ticket items can mean a lot more money to spend (and save) in other places.??

Having a moderate income does not mean that you have to live like a pauper.? If you want to live well, then the key is living within your means.? That means not stretching the family budget to upgrade to a larger home that you can barely afford, or trading up for a new car every few years.? A few small sacrifices here and there on your more big ticket items can mean a lot more money to spend (and save) in other places.??

If you find yourself tempted to “upgrade” homes, consider why you are looking.? If you simply do not have enough room for everyone, then think twice about how your home is currently arranged.? Does everyone have to have their own room?? Do you really need a room dedicated to being an office or an exercise room?? If you can combine spaces to make things work in a smaller home, then you can spend the money that would have gone to a larger mortgage payment on other things that will bring you much more immediate and hopefully lasting joy.??

The same goes for upgrading your car.? You may want to drive the newest model, but it obviously doesn’t keep you happy for long, or you wouldn’t feel the urge to upgrade.? Instead, pick a model that you love and stick with it.? Bonus points for picking a model that is moderately priced and that will save you money on gas in the long run, too.?

Spending quality time and living well does not have to involve spending a lot of money.? If you find yourself going out to dinner or to the movies often, then think about why you are going out and see if you can change your attitude to change your behavior.? You may find that taking a walk to the local park or spending time on your bike is not only healthier, but less expensive and just as enjoyable as spending money.? If you don’t cook your own meals because you don’t know how, then consider taking a cooking class - which you can consider an investment in yourself for the future.??

When you love to spend money, you should also never underestimate the power of the coupon.? If you have to shop, then save as much money as possible doing it by applying coupons and even using cash back rewards cards.? You should always make sure to pay your cards off in full when you get the bill to ensure that your interest does not negate the cash back.? Enjoy your spending, but do it wisely.??

It is easy to live well if you are living within your means.? “Keeping up with the Joneses” is a practice that is guaranteed to get you into financial trouble very quickly, but if you learn to enjoy the things that you can afford to have and to do, you will find that your life is already incredibly rich.?

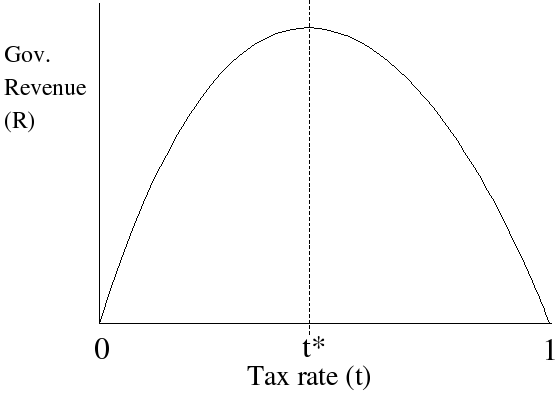

In 1973 Richard Nixon, US president, under political pressure because of rising domestic food prices, banned the export of soyabeans. The policy had predictably dire results, but today, with the world in the grip of another bout of food price inflation, governments worldwide are rushing to distort the market with subsidies and quotas, price controls and export taxes. They should stop.

In the run-up to its presidential election, Russia has imposed price controls on basic foodstuffs, and plans an export tariff on wheat. China already controls prices; other importers, including Egypt, Jordan, Bangladesh and Morocco, are increasing subsidies or fiddling with their tariff regimes.

The simple problem with all these actions is that they distort the market. Price controls and export tariffs make production less profitable, which discourages increased supply and can make shortages worse. Subsidies stimulate demand so it does not fall into line with higher prices. All distort the terms of trade within a country. Farmers suffer at the expense of city dwellers – especially perverse in countries with high rural poverty, such as China.

None of this is too bad in the short term. If food prices fall back, price controls become meaningless, subsidies can be withdrawn and export tariffs no longer make sense. The more pernicious problems will appear if food prices stay high. With more demand for protein from fast-growing Asian middle classes, lunatic policies to subsidise corn-based ethanol and the legacy of underinvestment during long years of low prices, that prospect seems likely.

For exporters, distorting the market in favour of domestic consumers harms the balance of payments, lowers investment and helps rivals. Nixon’s ban is often credited with creating Brazil’s soyabean industry.

For net food importers, who can keep prices down without shortages only by offering subsides, the risks are much more serious. Cheap food is an open-ended fiscal commitment – once in place it is politically impossible to withdraw – that can play havoc with a budget. Developing countries have improved their fiscal position in recent years. They should not throw that away.

Rich countries, where food is a small part of total consumption, have less to worry about, although they should beware the ratchet effect as food importers increase subsidies and food producers tax exports, driving up world market prices still further. But leaders in the developing world, no matter the political pressure to bring down the cost of grain, should resist. Cheap food comes at a high price.

{kind=link}